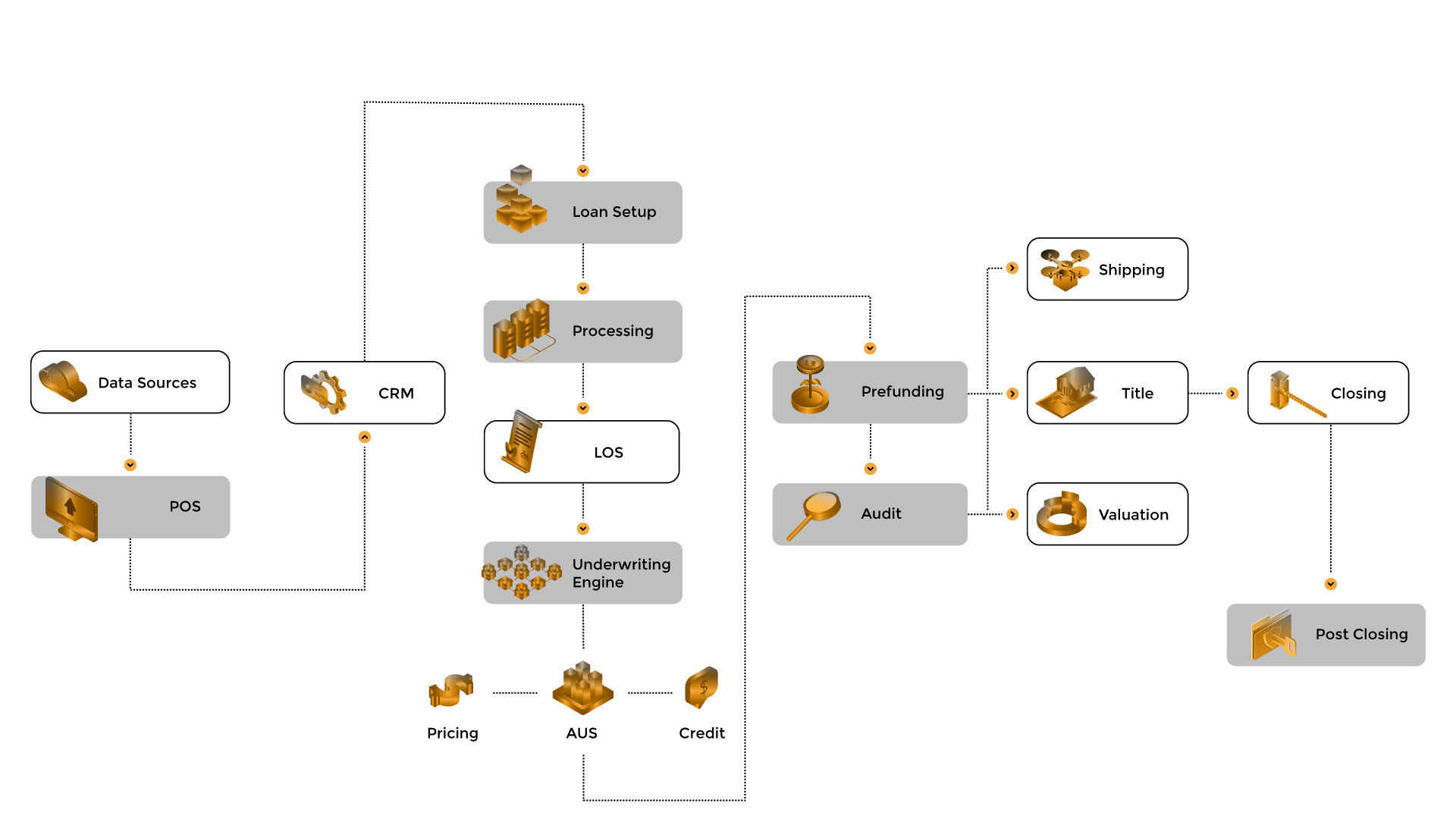

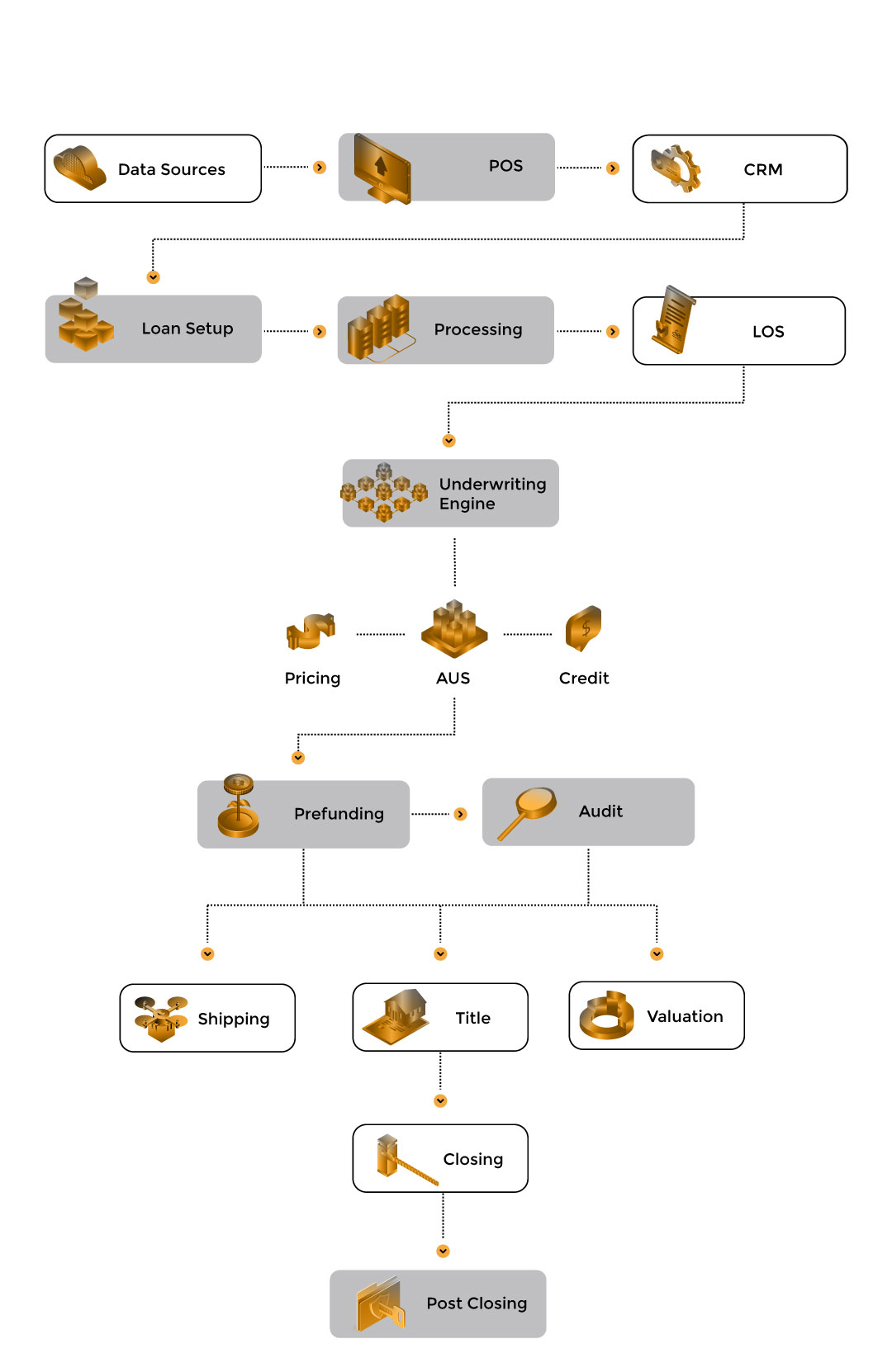

Applications based mortgage

Leverages AI-based engines to improve document processing capabilities with enhanced speed and accuracy

Mortgage underwriting

Utilizes the AI engine to simplify mortgage underwriting to provide the accurate and relevant information for the underwriters to take a faster decision and save cost.

Mortgage Appraisals and Valuation

Analyze mortgage valuations with more precision and helping faster processing of mortgage documents.

Reporting and Analysis

Reports anomalies and information gaps with increased efficiency and improve submission of compliance reports such as HMDA

Case Studies

How DocVu.AI Revolutionized ‘Order to Cash Process’ for a Leading Pharma Chain

Please submit this form to download Case Study

Case Studies

Bank in North America to Achieve Excellence in Post-Close Audit using IDP solutions

Please submit this form to download Case Study

Article

DMSVu vs. traditional DMS: A paradigm shift in document automation

In the relentless world of mortgage lending, document chaos is the enemy within. A recent Forbes report laid bare the

Article

7 emerging trends redefining post-closing audits in the digital mortgage era

When Wells Fargo disclosed a $37 million regulatory penalty in Q1 2024 due to post-closing audit failures, as reported by

Article

How cloud-based document management enhances security and scalability in finance & accounting

In April 2024, Bloomberg revealed a 45% year-over-year surge in cyberattacks targeting financial institutions still reliant on on-premise document systems,